The U.S. retirement system is about to experience some changes again. This news can make people who are planning to retire happy or disappointed and make them turn to extreme methods such as using legit money app or taking out loans.

New provisions connected with retirement in the form of “Secure 2.0” are included in the document, which comprises 4,100 pages.

It is a collection of provisions mentioned to build upon the improvements in the American retirement system. These improvements were earlier implemented under the Secure Act of 2019, hence the name of the second part. In this article, we are going to talk about the Secure 2.0 Act and what updates and new provisions are included in it.

What Is Secure 2.0?

What does the name mean? This document is created on the basis of the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019. It is pending a law created to improve retirement savings accounts of Americans, including 401(k) and 403 (b)s.

The Senate and the House have their own versions of this Act. The Senate version of the document was introduced on May 20, 2021, and is still in the Senate Finance Committee. The House version was passed on March 29, 2022, having huge bipartisan support.

Though many parts of these bills are similar, there are also some differences that should be worked out. The new law enjoys significant bipartisan support in both chambers. From policy changes to technical updates, Secure 2.0 would improve savings in workplace plans and boost participation, as well as expand assistance to small business owners willing to help you not to borrow money from your phone and save something for retirement.

The new legislation would boost certain tax incentives for the economically secure. Hence, it is believed that this law will come into action in the nearest future.

Understanding the Secure 2.0

Both chambers of Congress wish Secure 2.0 to become a new law soon. Both versions of this bill have strong bipartisan support. The 103 sponsors of H.R. comprise 48 Republicans and 55 Democrats.

What goals does Secure 2.0 want to achieve? It is meant to accomplish three targets:

- Boost retirement regulations.

- Help Americans save more money for their comfortable retirement.

- Reduce the recruiter cost of creating a retirement plan.

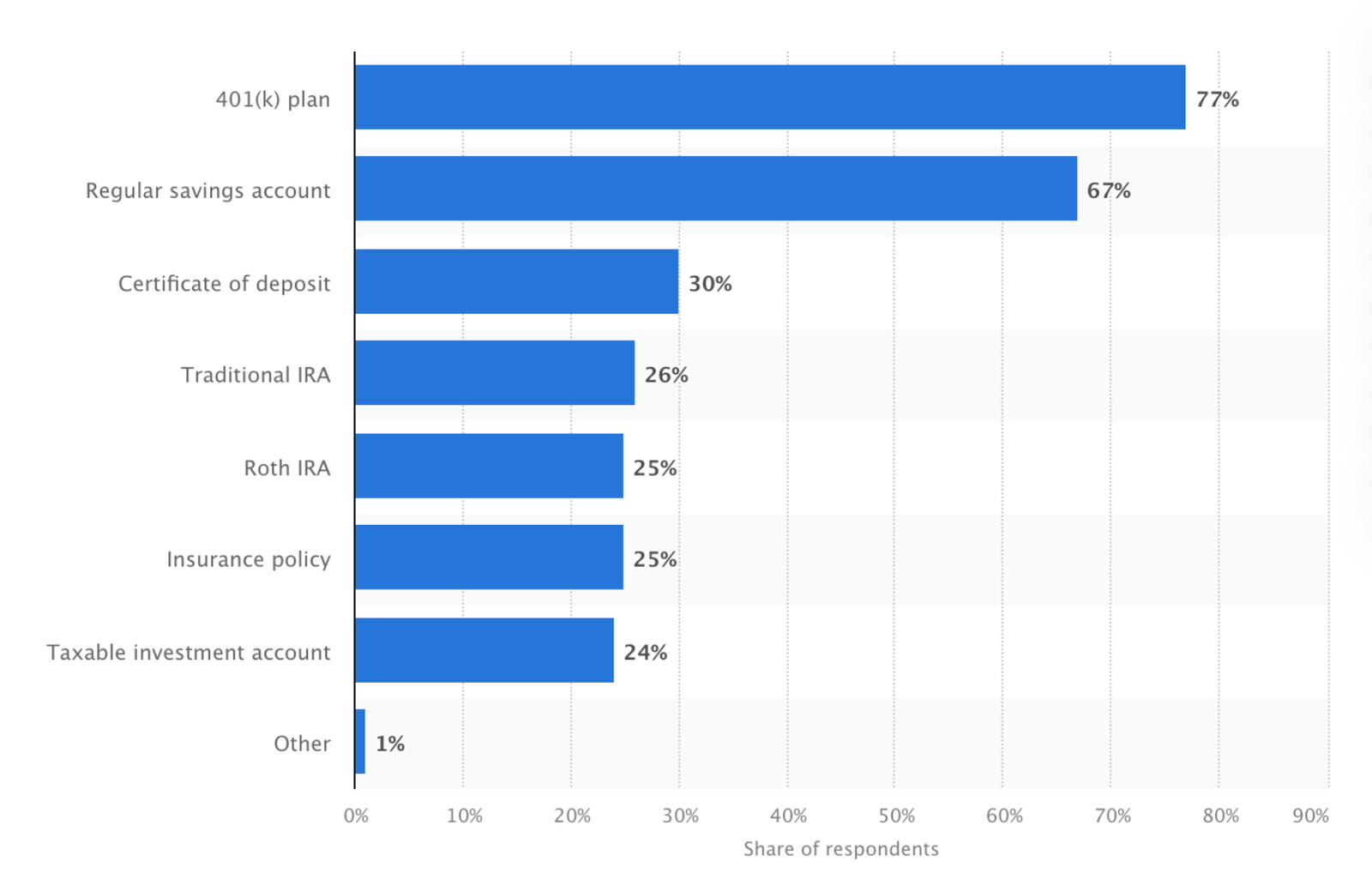

The statistics from 2021 show that the majority of surveyed Americans had a 401(k) plan for retirement (77 percent). The second most popular retirement savings account type was a regular one (67 percent). Thirty percent of respondents had a certificate of deposit, while less than a third of surveyed Americans utilized the rest of the accounts.

What is the most popular provision of this document? It is probably the one allowing recruiters to provide matching retirement contributions to workers repaying their student loan debt. Recruiters will get employer matching contributions if they agree to make student loan payments rather than contribute to the company’s 401(k) account.

Which Provisions Are Included

- Demanding automatic 401(k) enrollment. Recruiters would be demanded to automatically enroll their workers in their 401(k) plan at a rate of at least 3%. This rate shouldn’t be over 10% as well. New startups and companies with ten or fewer employees would be excluded from this provision.

- Making larger “catch-up” contributions for older savers. Americans have the right to put an additional $6,500 yearly in their 401(k) when they reach age 50. The new Secure 2.0 law would increase these limitations to $10,000 beginning in 2025 for older retirement savers aged 60 to 63. More than that, all contributions would fall into Roth treatment unless you earn $145,000 or less.

- Raise the age when RMDs should begin. The present bill would enhance it from age 72 to 73 in the coming year. Later, this age will be raised to 75 in 2033. Furthermore, the penalty for not taking RMDs would be lowered to 25% or 10%.

- Boosting employee access to the emergency fund. Not many workers have enough savings in their emergency fund. So, thousands of Americans rely on credit tools and loans. One of the provisions of this bill would allow workers to withdraw $1,000 or less from their retirement fund to cover emergency costs. They won’t have to pay a 10% tax penalty for such an early withdrawal, provided they are up to age 59 ½. Automatic paycheck deductions may also be utilized to help employees establish their emergency fund, with a cap of $2,500.

- Developing employer 401(k) match options. A new bill would enable recruiters to make contributions to 401(k) plans instead of their workers who are repaying student loan debt. So, employees wouldn’t need to cope with student loan debt payoff and saving for their retirement at the same time.

- Boosting part-time employees’ access to retirement funds. According to the previous 2019 Secure Act, part-time workers who book from 500 to 999 hours for three years would qualify for their company’s 401(k). The new Secure 2.0 bill lowers this requirement to two consecutive years. Businesses have already been demanded to give access to workers who have at least 1,000 working hours in a year.

- Increasing uses for unutilized college savings funds. The new Secure 2.0 Act would let penalty- and tax-free rollovers from 529 college savings accounts to Roth IRAs under particular conditions.

- Altering the demanded minimum distributions rules for Roth 401(k)s. Nowadays, Roth IRAs have no RMDs for the initial account owner’s life. The pre-death distribution demand will be canceled starting in 2024.

- Increasing the sum that can be placed in a qualified longevity annuity contract. You may put a maximum of $135,000 or 25% of the retirement account’s value into a QLAC account. The new bill is meant to cancel the 25% requirement and boost the maximum sum allowed to be put in a QLAC up to $200,000.

The Bottom Line

In conclusion, Secure 2.0 presents a document of provisions created to build upon improvements to the American retirement system implemented under the Secure Act of 2019. Those updates included boosting the age when required minimum distributions must begin – to age 72 from 70 ½ as well as offering part-time employees better access to retirement benefits. Secure 2.0 is a paper both chambers of Congress wish to see become a new law, as both versions have strong bipartisan support.

{kind=link}